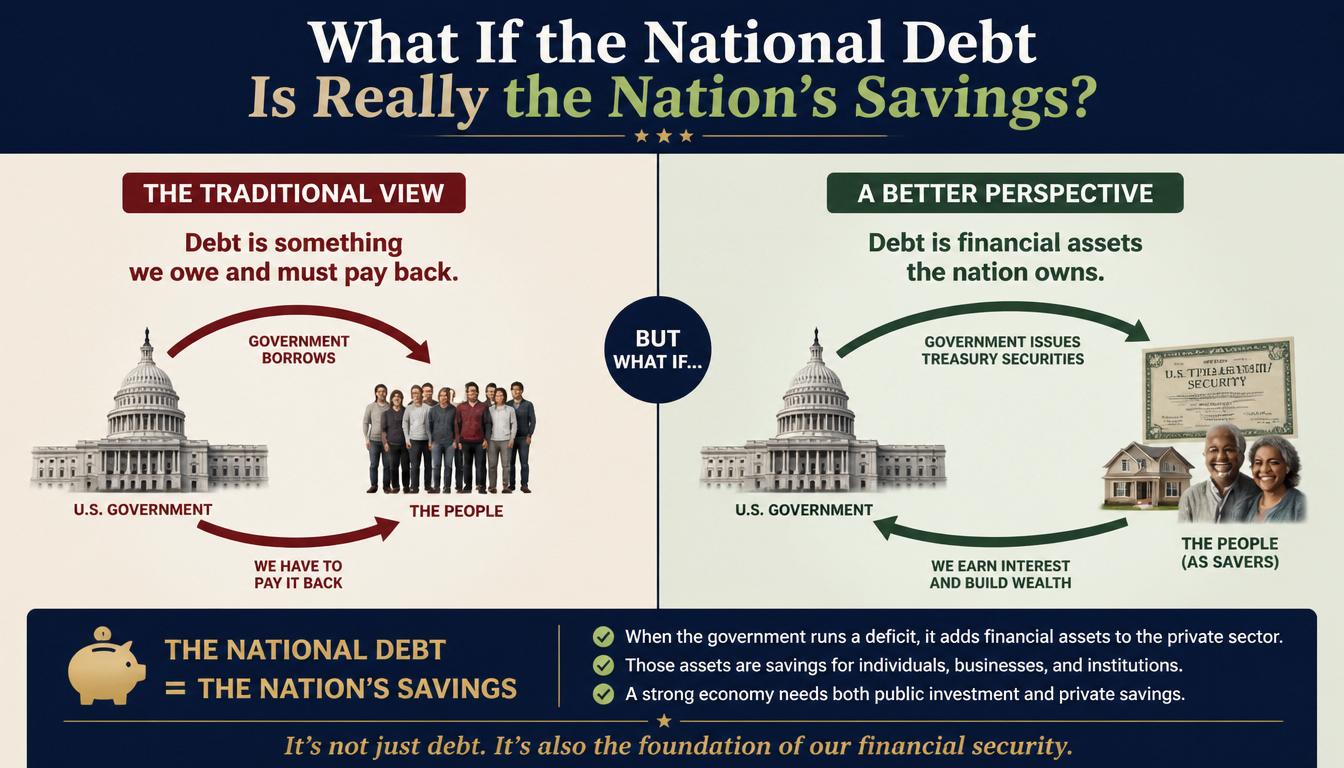

What if the national debt is not a burden at all? What if it is simply the nation's savings? Any sensible look at the figures shows that the so-called debt is no such thing — it is a vast savings-bank operation, and almost nothing else.

That sounds like a contradiction, but it is not. And understanding why changes almost everything about how we think about government finance, public spending, austerity and economic policy. The argument is simple to state and surprisingly hard to dislodge once you have seen it: every pound of government debt is also somebody else's financial asset. Government bonds are not really debt in the way a household understands debt. They are savings accounts held with the state, and the financial system depends on them utterly.

Pension funds, insurance companies, banks and many of the world's largest investors all rely on UK government bonds as the safest place to hold their wealth. So before we accept the idea that the country must one day “pay off the national debt,” it is worth asking what we would actually be paying off — and to whom. The same dynamic shapes sterling on the FX market, the FTSE on the index desks, and the rate-sensitive corners of commodities and UK stocks.

01 / A Category Error — Calling bonds “debt” distorts the whole debate

When anyone buys a government bond — a “gilt,” as we call them in the UK — they are simply placing money on deposit with the government. The government is not, in any meaningful sense, borrowing their money in the way you borrow for a mortgage. It is holding their savings in the safest place that exists. A gilt is, in principle, no different from a national savings account. In fact, that is what they ought to be called.

Here is the accounting fact that the word “debt” hides from us. All savings deposits are liabilities of whoever holds them. When you deposit money in a bank, that deposit appears on the bank's balance sheet as a liability — money it owes back to you. We do not say the bank is in crisis because it “owes” its depositors their money. So why do we say the government is in crisis because it owes savers theirs? It is exactly the same relationship, dressed in frightening language.

Think about what sits on a bank's balance sheet. Its major liabilities come in two kinds. One is loan finance — money genuinely lent to the bank so it can do business. The other is deposit accounts — and these are not money the bank needs in order to operate. We know this because banks can, and do, lend without first taking in a matching deposit. This is not a controversial claim; it is the Bank of England's own position, set out plainly in its 2014 study of how money is created in a modern economy. The government, likewise, takes deposits it does not need. It accepts them as a service to the world, not as a necessity for itself.

What we accept calmly

You → Bank

Your deposit is…

YOUR ASSET (savings)

BANK'S LIABILITY (owed back to you)

“Nobody panics.”

What we fear

You → Government

Your gilt is…

YOUR ASSET (savings)

GOV'T LIABILITY “the national debt”

“Everybody panics.”

A bank deposit and a gilt are the same kind of thing: an asset for the saver, a liability for the institution. We have simply chosen to call one “savings” and the other “debt” — and only the second word frightens us.

02 / The Twist — A government that issues its own currency cannot go broke

But there is a crucial twist that separates a government from a bank. Banks can fail. The UK government has never once failed to repay a gilt — not in the entire history of the national debt, which stretches back unbroken to the founding of the Bank of England in 1694, through the Napoleonic Wars and two world wars, with debt at times far higher, relative to the economy, than it is today.

The reason is straightforward. The UK issues its own currency and has its own central bank. It can always create the money it needs to settle its bonds as they fall due. It does not need to borrow in order to repay, because why would an entity that can create money at will ever be unable to find it? This is the heart of what economists call monetary sovereignty, and it is precisely the point Stephanie Kelton makes in The Deficit Myth: a government that issues its own non-convertible currency, and borrows only in that currency, simply does not face the budget constraint that a household does.

We already rely on this fact every single day, even if we have never named it. Consider the bank deposit guarantee. As of December 2025, the government guarantees up to £120,000 of your savings in any failed UK bank. How can it make that promise good even if the bank itself cannot? Only because we all implicitly understand that the government can create the money to honour it. So let us stop pretending we do not know that governments can create money. The entire architecture of our financial confidence rests on the knowledge that they can.

A currency-issuing government is not like a household, and it is not even like a bank that can go broke. Treating gilts like a household mortgage is a fundamental mistake — and it is the mistake on which decades of austerity were built (see The City Is Holding Britain Hostage).

And notice how that deposit guarantee actually points us towards why bonds exist at all. The guarantee covers £120,000. But suppose a corporation, a pension fund or a foreign government wishes to place a billion pounds somewhere safe overnight. For them, a guarantee capped at £120,000 is worthless. So the government provides bonds instead: a place where institutions can park enormous sums in perfect safety. That is the real function of the gilt market. It is not the government begging for funds. It is the government supplying the world with the safe asset it desperately needs.

03 / Who Actually “Lends” to the Government

If you want proof that the national debt is really national savings, look at who holds it. These are not reckless creditors holding a government to ransom. They are the most safety-obsessed institutions in the economy, using gilts for exactly the purpose a savings account serves.

| Holder | Share | Why they hold them |

|---|---|---|

| Overseas investors & governments | ~33% | A safe global store of value in sterling. |

| Insurance companies & pension funds | ~21% | To match long-term promises to savers and pensioners. |

| Bank of England (Asset Purchase Facility) | ~18% | The state holding its own liability — via QE. |

| Banks & other financial institutions | ~the rest | The bedrock safe asset of the money markets. |

| — incl. NS&I, held by ordinary savers | ~£230bn+ | Premium Bonds and savings, 24m+ customers. |

Sources: DMO / ONS / Bank of England gilt-holding data; NS&I Annual Report 2024–25.

Look closely at that last line. Around £230 billion or more of the so-called national debt is simply National Savings & Investments — Premium Bonds and savings accounts held by more than twenty-four million ordinary British people. NS&I literally describes itself as “the nation's savings bank.” Nobody believes their Premium Bonds are a sinister burden on the next generation. Yet they are part of the very number politicians tell us we must one day eliminate.

And here is the part the City of London understands perfectly well, even as it nods along to the politicians. Without gilts, the banks, the money markets, the insurers and the pension funds could not function. They are all critically dependent on government bonds as an essential tool of their daily commercial operations — as collateral, as a safe asset, as the risk-free benchmark against which everything else is priced. The national debt is the foundation the whole financial system is built on.

So what would it actually mean to “pay off the national debt”? It would mean forcing all those savings to go somewhere else — somewhere less safe, possibly outside the UK, certainly riskier — and pulling the foundation out from under the banks, the money markets and the pension funds we cannot do without. The idea is not merely unnecessary. It is absurd.

Viewed from the government's side…

“THE NATIONAL DEBT”

→ ONE & THE SAME POUND ←

“THE NATION'S SAVINGS”

…viewed from the saver's side

It is a single quantity of money. Call it from one end and it sounds like a millstone; call it from the other and it is a pension, an insurance reserve, a corporate treasury, a Premium Bond. Same pound, two names.

04 / The Myth of the Bond Vigilante

This brings us to one of the most powerful pieces of theatre in modern politics: the idea that “bond vigilantes” hold governments to account — that shadowy financiers at pension funds, banks and hedge funds enforce fiscal discipline by punishing any government that displeases them. It is, in the main, nonsense.

These people are not guardians of sound public finance. They are traders. They buy and sell government bonds to make a profit, and that is the entire extent of their interest. They are not lying awake worrying about the long-run health of the public finances; they are looking for the chance to buy low and sell high. They do not enforce good economic management as they see it, and no one should pretend they do.

The deeper reason the vigilante story fails is mechanical. In this country, the Bank of England sets the base rate, and the evidence shows that bond yields track that rate — bond dealers do not set it. When yields rise and bond prices fall, the central bank can always step into the market and buy bonds in whatever quantity it chooses to bring yields back down. This is routine. It is called an open market operation, and it has gone on for decades. Quantitative easing during the 2008 financial crisis and again during the pandemic proved the point on a colossal scale: at its peak the Bank of England held a target stock of £875 billion of gilts. When the state decides to set the price of its own debt, it can.

05 / But What About 2022?

At this point a fair-minded reader will object: what about September 2022? The “mini-budget,” the spike in yields, the run on the pound, the Bank of England forced to intervene, the Prime Minister gone within weeks. Surely that is the bond market disciplining a government in real time?

It is the strongest counterexample, and it deserves an honest answer rather than a dismissal — because when you look at what actually happened, it does not vindicate the vigilante story. It quietly confirms the opposite.

Start with the cause. The crisis was not a sober verdict by disciplined investors. It was a plumbing failure. For years, defined-benefit pension funds had been running highly leveraged “liability-driven investment” (LDI) strategies — in effect, borrowing against gilts to buy more gilts. When yields jumped after the mini-budget, those leveraged funds faced margin calls, were forced to sell gilts to raise cash, which pushed yields higher still, which triggered more selling: a doom loop. The Bank of England's own researchers later estimated that this forced LDI selling accounted for roughly half of the entire fall in gilt prices — with the fiscal announcement responsible for the rest. This was a fire in the private sector's own leveraged machinery, not a calm act of market discipline.

| The “vigilante” story says… | What the evidence shows |

|---|---|

| Disciplined investors judged the government and sold. | ~50% of the price fall came from forced, mechanical LDI selling — a leverage accident, not a verdict (BoE research). |

| The market was in control. | The Bank intervened for just 13 days, buying £19.3bn of long-dated gilts, and the freefall stopped. The state set the price. |

| Markets enforce sound policy. | They did not prevent the leverage building up for a decade under the regulator's nose; they only convulsed once it broke. |

Sources: Bank of England, “What caused the LDI crisis?” (Bank Underground, 2024); BoE financial-stability intervention figures, Sept–Oct 2022.

Now look at the resolution, because it is decisive. How was the largest, most sophisticated bond market in Europe pulled back from the brink? The currency issuer stepped in. The Bank of England's emergency operation lasted a mere thirteen days and bought just over nineteen billion pounds of long-dated gilts — a modest sum in that market — and the panic subsided. That is the whole argument in miniature. The instant the state chose to act, it set the price. Far from proving that bond markets control the government, 2022 proved that when it matters, the government controls the bond market. The vigilantes were not the firefighters. They were the fire.

06 / Why the Myth Persists

So why do politicians, including those in the Labour Party who now live in visible fear of the City, keep talking about bonds as a debt that must be repaid? Partly because they have never understood what bonds are; the household analogy is so intuitive that most cannot think past the limits of their own kitchen table. And partly — let us be honest — because the myth is useful.

If you wish to cut public spending, the belief that “the debt must be repaid” is the perfect justification. It manufactures a crisis that demands austerity as the cure. This is why the idea is promoted so energetically by those who wanted austerity anyway: it lets them present something socially useful — a vast, safe savings facility that underpins the whole economy — as a danger to be eliminated. Never lose sight of that true agenda. The fear of government bonds is manufactured, and it can be refused. The language of “debt burden” and “crisis” is political, not economic. The companion essay The City Will Never Fund Small Business traces the same political economy from the opposite end — the glut of idle savings the City refuses to deploy.

Here, finally, is the honest caveat I promised. The genuine limit on a currency-issuing government is not bankruptcy — that cannot happen — but inflation. If a government spends far beyond the real capacity of the economy to produce goods and services, the result is rising prices, not insolvency. This is the serious objection mainstream economists raise against Modern Monetary Theory, and it is a real one. But notice that it is a completely different problem from the one we are usually frightened with. The right question is not “how do we repay the debt?” — that question is meaningless. The right question is “how do we manage the nation's savings, and the real economy behind them, well?”

| “Debt” framing | “Savings” framing | |

|---|---|---|

| What it is | A burden owed | Private wealth held safely with the state |

| The goal | Reduce it / “pay it off” | Manage it well |

| Who's in control | The bond markets | The currency issuer (the state) |

| The real constraint | Running out of money | Inflation / real economic capacity |

| Policy it justifies | Austerity | Investment |

The choice of framing is not a technical footnote. It silently determines which economic policies look “responsible.”

If the national debt is really national savings, the whole debate has to start somewhere new.

Every time a politician warns us about the bond markets, they are accepting a false premise — and accepting it has consequences. It has justified decades of unnecessary austerity, chronic underinvestment, and a permanent, manufactured fear of public spending. Getting this right is not a technical nicety. It is a precondition for competent government.

Bonds are a savings facility that the economy depends upon. The real question was never how to shrink that facility, but how to run it well — and governments that understand this are never truly constrained by the bond markets at all. The fear has been manufactured. We are free to set it down.

Frequently asked questions

Is the national debt really the nation's savings?

Yes — in accounting terms, every pound of UK government debt is somebody else's financial asset. Gilts are deposits held with the state by pension funds, insurers, banks, overseas investors and ordinary savers via NS&I. The government's liability is the saver's asset. They are the same pound, viewed from two sides.

Can the UK government go bankrupt?

No. The UK issues its own non-convertible currency (sterling) and has its own central bank. It can always create the money it needs to settle gilts as they fall due. In over 300 years — including the Napoleonic Wars and both World Wars — it has never defaulted on sterling debt. The real constraint is inflation, not insolvency.

Who holds the UK national debt?

Roughly 33% is held by overseas investors and governments, ~21% by UK insurance companies and pension funds, ~18% by the Bank of England via the Asset Purchase Facility, with the remainder held by banks and other financial institutions. Over £230bn sits with National Savings & Investments — Premium Bonds and savings held by 24m+ ordinary British savers.

What is Modern Monetary Theory (MMT)?

MMT, associated with economists Stephanie Kelton, Warren Mosler and L. Randall Wray, argues that a government that issues its own currency cannot run out of money — its real constraint is the productive capacity of the economy, expressed through inflation. Kelton's 'The Deficit Myth' is its best-known popular statement.

What actually caused the September 2022 UK gilt crisis?

The Bank of England's own research found that roughly half of the price fall came from forced, mechanical selling by leveraged LDI pension strategies — a plumbing failure, not a verdict. The Bank intervened for just 13 days, buying £19.3bn of long-dated gilts, and the freefall stopped.

How does this affect traders and the markets?

Understanding bonds as savings — not debt — reframes how gilt yields, sterling and UK equity indices respond to fiscal headlines. Yields are anchored by Bank Rate and central-bank operations. MT5 Viper Strategy non-repainting signals are built to trade the macro-driven moves these dynamics produce across forex, indices and commodities.

Further reading on this site

For the companion essays on the political economy of UK money, see The City Is Holding Britain Hostage and The City Will Never Fund Small Business. For how this macro backdrop shows up in the markets traders actually trade, see our pages on forex, indices, commodities and UK stocks. If you want to translate macro into a repeatable process, start with developing a trading strategy and how to backtest in MT5. For the funded-trader angle, see the great migration from forex to futures prop firms and how prop firms detect algorithmic trading in 2026. Ongoing macro is tracked on trending topics.